Why Israel’s stock market is becoming harder to ignore

")

For years, Israel’s economy and its stock market appeared to exist in parallel rather than together. The country developed a global reputation in cybersecurity, software, and advanced technology, yet international investors often preferred gaining exposure to Israeli companies through Nasdaq rather than through the Tel Aviv Stock Exchange (TASE) itself.

That distinction is becoming harder to maintain.

The recent evolution of the Tel Aviv Stock Exchange suggests that Israel’s capital market is beginning to catch up with the sophistication of the economy behind it. Liquidity is improving, foreign participation is rising, and market reforms are gradually reducing some of the operational frictions that historically discouraged larger institutional investors.

The numbers are increasingly difficult to dismiss.

The exchange reported a first-quarter 2026 revenue of NIS 183.3 million (USD $63 million), up 40% from a year earlier and the highest quarterly figure since its initial public offering. Net profit rose 116% to NIS 77.4 million (USD $26.5 million), while underlying operating profit increased 87% to NIS 115.6 million (nearly USD $40 million).

Exchanges are effectively leveraged reflections of market activity. When trading volumes, listings, and custody assets rise simultaneously, it usually indicates improving participation across the broader financial system rather than isolated speculative enthusiasm.

That appears to be what is happening in Israel.

Average daily share trading volumes reached NIS 5.6 billion (USD $1.9 billion) during the first quarter, compared with NIS 2.9 billion (USD $1 billion) a year earlier – a 92% increase. Total share market capitalization climbed to approximately NIS 2.543 trillion (USD $872.5 billion), up 86% year-on-year.

These are not the figures of a marginal market struggling for relevance. They are the figures of a market becoming increasingly usable for institutional capital.

One of the most important changes was also one of the least dramatic. At the beginning of 2026, Israel completed the transition from its historic Sunday-to-Thursday trading week to a Monday-to-Friday schedule.

The reform sounds administrative. In practice, it removed a persistent obstacle for international investors. Under the previous calendar, portfolio managers in London and New York operated with limited overlap with Israeli markets, complicating execution and hedging. The new structure aligns TASE more closely with global trading patterns.

The effect was immediate. According to TASE management, average Friday trading volumes reached NIS 4.4 billion (USD $1.5 billion) following the transition, compared with average Sunday volumes of NIS 1.6 billion (USD $5.5 million) previously. Foreign participation also increased.

Operational convenience may not sound exciting, but global finance is heavily dependent on infrastructure. Investors rarely allocate substantial capital to markets that are operationally awkward, regardless of the underlying economic story.

Israel’s broader economic resilience is reinforcing the shift. The shekel has strengthened sharply against the US dollar over the past year despite continued regional conflict. That has challenged a long-standing assumption that geopolitical risk must inevitably weaken Israeli assets.

Currency markets are rarely ideological. A strengthening currency generally reflects confidence in capital flows, economic resilience, and long-term investment prospects. In Israel’s case, the shekel’s performance increasingly suggests that foreign investors are looking beyond short-term geopolitical headlines.

Increasingly, investors are gaining exposure not only to Israeli companies but also to an economy with competitive strengths in sectors becoming strategically important globally.

Israel offers concentrated exposure to industries where it holds genuine competitive advantages: cybersecurity, defense technology, financial services, energy infrastructure, and advanced software. In a world increasingly shaped by digital security, military rearmament, and artificial intelligence, those sectors are attracting growing investor attention.

Cybersecurity remains one of the strongest pillars supporting international interest in Israeli equities. “The cybersecurity market is currently in its golden age,” said Adv. Guy Lachmann, partner and co-head of the Israeli high-tech practice at Pearl Cohen. He cited the expansion of artificial intelligence, rising defense spending and growing demand for digital protection. He added that Israeli companies continue to command a premium because of the country’s reputation as a global leader in cybersecurity.

The composition of the Israeli market is therefore becoming more relevant internationally.

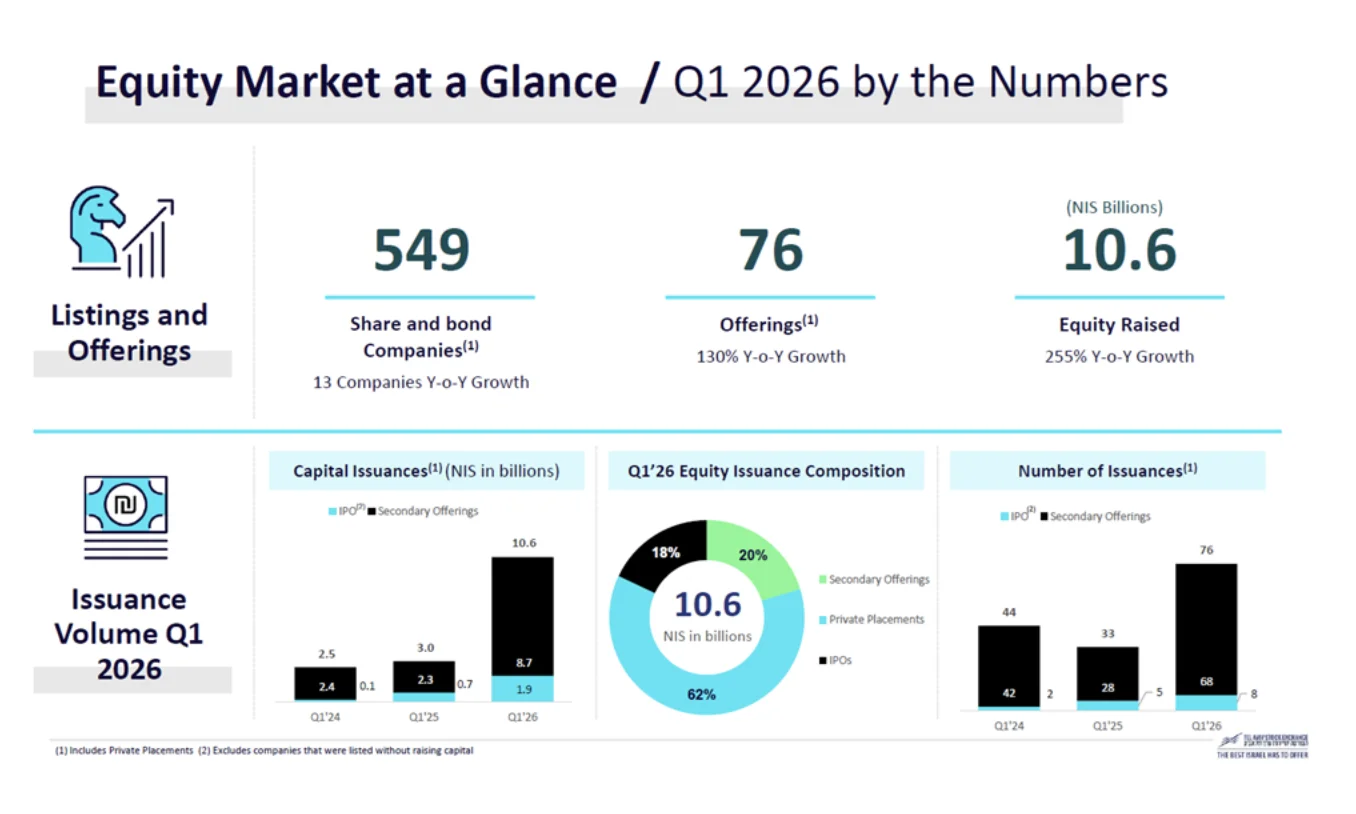

That is visible not only in trading activity but also in capital raising. Companies raised NIS 10.6 billion (USD $3.6 billion) through equity offerings during the first quarter of 2026, up 255% from the same period a year earlier, while the number of offerings rose 130% to 76.

Public holdings in foreign exchange traded funds listed on TASE rose to NIS 19.6 billion (USD $6.7 billion) during the quarter, approximately NIS 4.5 billion (USD $1.54 billion) higher than a year earlier. The primary market also showed signs of renewed activity. Eight companies completed IPOs on the exchange during the quarter, raising NIS 1.9 billion (USD $652 million) compared with five flotations that raised NIS 700 million (USD $2.4 million) during the same period in 2025.

Ittai Ben-Zeev, Chief Executive of TASE, said the exchange is also seeing growing interest from private companies considering future listings, suggesting that improving liquidity conditions are building confidence in the local market.

The shift is becoming increasingly visible among larger technology companies as well.

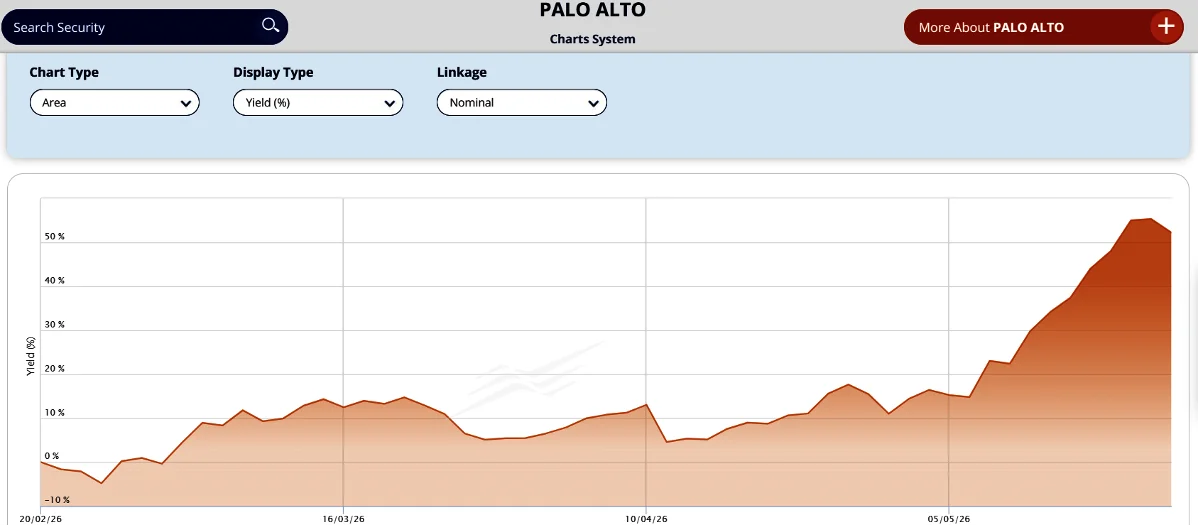

Palo Alto Networks’ decision to pursue a dual listing in Tel Aviv following its acquisition of CyberArk was symbolically important. Since beginning trading on TASE on Feb. 20, the stock has already risen by more than 50%. The strong performance reflects both investor demand for cybersecurity exposure and growing confidence in the exchange’s ability to host globally recognized technology companies.

Calcalist reported that eToro’s board is considering a potential dual listing in Tel Aviv less than a year after the company’s Nasdaq debut. If completed, the move would reinforce the growing credibility of TASE among internationally recognized Israeli technology companies.

Liquidity improvements extend beyond equities.

Corporate bond trading volumes rose 34% year-over-year during the first quarter, while government bond trading increased 39%. Treasury bill trading climbed 57%.

The derivatives market is expanding as well. Since the launch of TA-125 futures contracts in late 2024, monthly trading volumes reportedly increased from approximately 7,500 contracts to around 65,000 by March 2026.

These developments are important because institutional investors require hedging tools and sufficient market depth before allocating meaningful capital. Markets become investable not merely because of economic narratives but because the surrounding infrastructure allows capital to move efficiently.

The improving market backdrop does not eliminate Israel’s structural vulnerabilities. Israel remains exposed to geopolitical shocks, currency volatility, and abrupt reversals in investor sentiment. Liquidity, although improving, still remains well below that of larger developed exchanges.

There is also a danger that enthusiasm surrounding defense and cybersecurity themes becomes excessive. Some parts of the market have rallied sharply over the past year, increasing the possibility of future corrections if expectations move ahead of fundamentals.

Still, the broader direction appears increasingly clear.

For years, Israel’s economy often appeared more globally important than its capital market infrastructure. International investors respected Israeli innovation while treating Israeli equities as secondary to US-listed alternatives.

That gap is narrowing.

The Tel Aviv Stock Exchange is becoming more liquid, more internationally aligned, and increasingly integrated into global capital flows. Israel may still not occupy the same position as the largest developed markets. But the combination of stronger liquidity, growing institutional participation, and expanding technology representation is making it progressively more difficult for global investors to treat the market as peripheral.

Ihor Pletenets is a finance professional with over 14 years of experience in capital markets across the UK and Israel. He holds a B.A. (Hons) in Accounting and Finance from the University of West London, where his interest in investing first began.

He is the author of The Money Lessons You Wish You Learned in School, a practical guide to investing and personal finance. Drawing on his experience in the financial industry, he writes on financial markets, economic trends, and investing.

You might also like to read this:

")

")

")

")

")

")

")

")

")