War hasn’t broken Israel’s markets – it’s strengthened the investment case

")

The case for Israel is not subtle. It runs against instinct. War, political noise, and regional volatility should, in theory, push capital away. Yet over the past two and a half years, the opposite has happened: the currency has strengthened, equities have risen, and foreign capital has continued to flow. For investors, that gap between expectation and reality is where the opportunity lies.

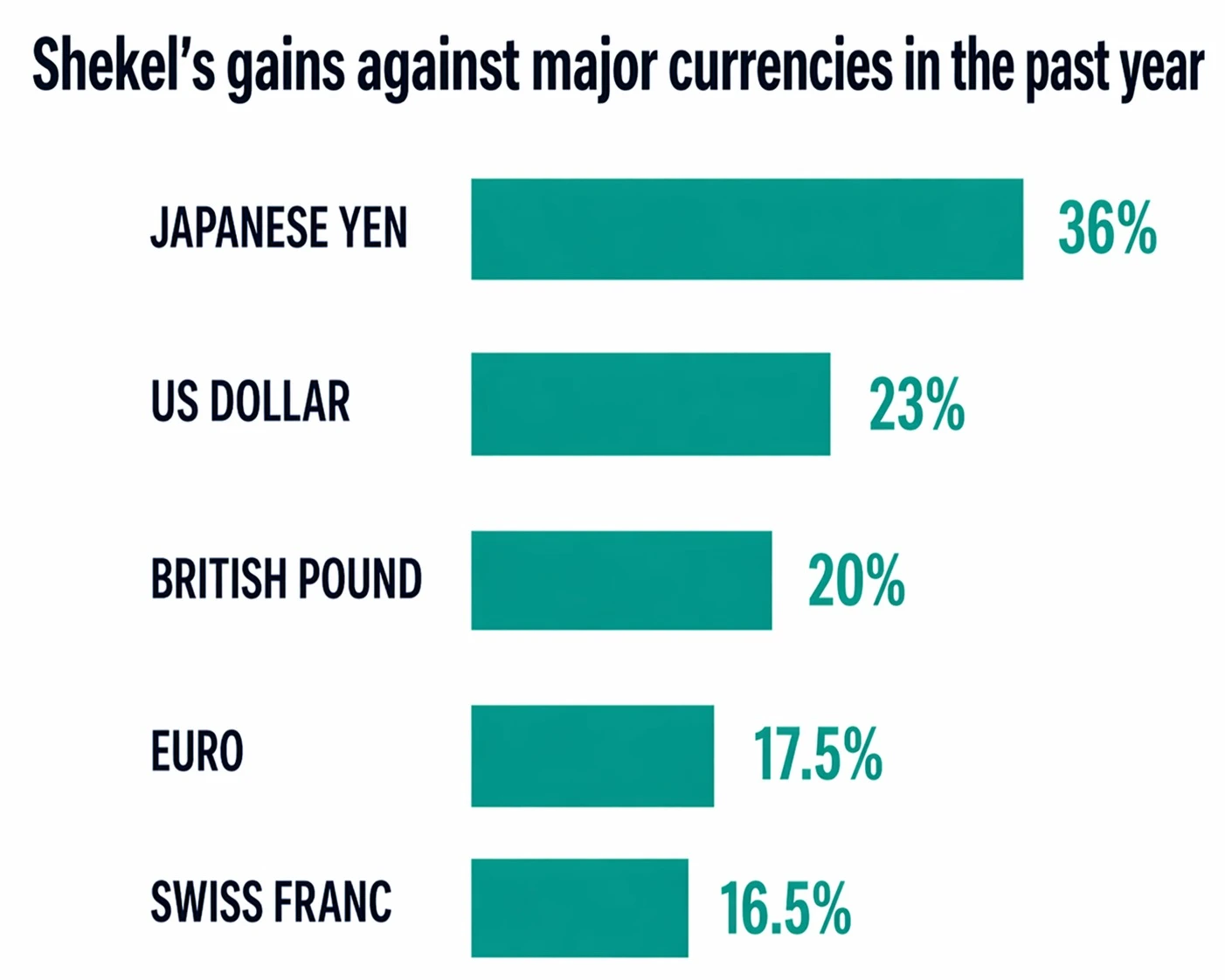

Start with the currency. The shekel has appreciated sharply – by more than 20% against the dollar over roughly the past 18 months – even as Israel remained engaged in a prolonged, multi-front conflict. This is not a technical move driven by a weakening dollar alone. The shekel has also strengthened against a broader basket of currencies, pointing to underlying demand rather than relative weakness elsewhere.

The drivers behind the move operate on multiple levels. As Ofer Klein, chief economist at Harel Insurance and Finance, has noted, longer-term factors such as trade flows, productivity and inflation gaps have combined with shorter-term influences – geopolitics and strong US equity markets prompting institutional dollar selling. The result is an unusual convergence, with multiple dynamics strengthening the shekel.

Israel’s macroeconomic performance reinforces the point. After expanding by more than 6% in 2022, GDP continued to grow in 2023 despite the outbreak of war in the final quarter and remained positive overall through 2024 even as parts of the economy contracted under mobilization and disruption. That stands in contrast to more acute wartime shocks elsewhere: Ukraine’s economy, for example, shrank by roughly 30% in 2022 following the Russian invasion.

The drivers are structural. Israel continues to run a current account surplus, supported by high-value exports in technology, cybersecurity, and defense systems. Foreign capital has not retreated, it has increased. Bank of Israel data show net foreign investment rising to around $39 billion in 2025 from $25 billion the year before. Large technology deals – such as Wiz sale to Google – and capital raises inject additional foreign currency into the system. Much of it is ultimately converted into shekels, sustaining demand for the local currency.

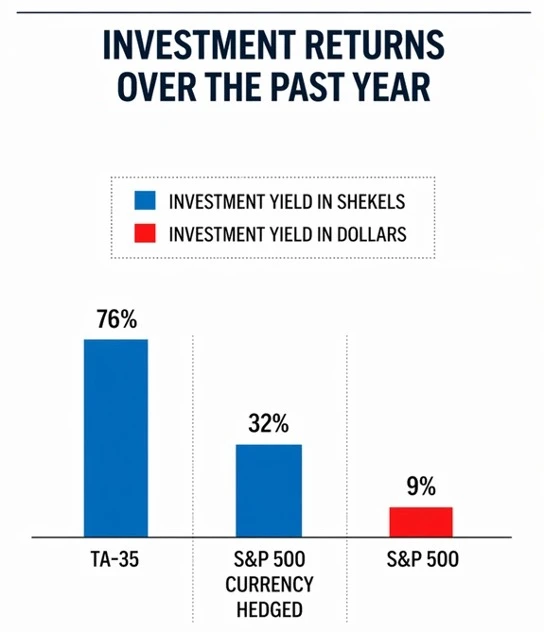

That matters because currency is not a sideshow to returns. It often is the return. The past year has exposed how easily investors can overlook that. The S&P 500 delivered 32% in dollar terms over the period. Yet for an Israeli investor measuring wealth in shekels, the over 20% depreciation of the dollar significantly eroded those gains.

The lesson is not to avoid U.S. equities. It is to recognize that currency exposure is an active decision, not a neutral one. Investors tend to think in assets – equities, bonds, alternatives – but often ignore the currency in which those assets are denominated.

In Israel’s case, that omission has been costly. As Edith Moskowitz, who oversees capital markets and foreign exchange trading at Beinleumi Bank, has noted, strong gains in dollar terms have translated into far more modest returns for local investors, as the appreciation of the shekel has negatively impacted those profits. Those without currency hedging, in particular, have often been left with only a fraction of the headline gains.

The equity market reflects the same underlying dynamics. Israeli indices have risen not on sentiment, but on sectoral strength tied to global demand. Cybersecurity remains a core pillar, with Israeli companies deeply embedded in enterprise systems worldwide. Demand here is structural rather than cyclical, driven by the necessity of defending digital infrastructure. The broader technology sector continues to attract foreign capital through acquisitions and funding rounds, reinforcing both valuations and foreign exchange inflows.

Defense technology has become more prominent. The past two years have increased both domestic demand and export interest in Israeli systems.

The Tel Aviv Stock Exchange responded by launching a dedicated defense index in November 2025, grouping companies exposed to military and security demand. It has risen by roughly 30% since inception, a sign that investors view the cycle as structural. In a market that increasingly values operational proof, equipment tested in real-world conditions carries weight. Much of the revenue generated by these companies is earned in foreign currency, feeding directly into export flows that support the shekel.

Put together, these sectors do more than drive equity performance. They anchor the currency. Export revenues, foreign investment, and capital market activity form a loop in which each reinforces the other. That coherence is what distinguishes Israel from many smaller markets, where equity gains can be detached from macroeconomic fundamentals.

Perhaps the most counterintuitive element is the persistence of foreign inflows. Extended conflict would normally deter capital. In practice, investors have continued to allocate to Israel. In a world where political and economic uncertainty is hardly confined to one region, investors weigh opportunities against alternatives, not against an idealized baseline. An economy that continues to generate growth, attract capital and maintain financial stability under stress tends to see its risk premium compress – a shift that is already visible in the continued inflow of capital.

None of this removes the risks. A strong currency carries costs. Rapid appreciation compresses exporters’ margins and can, over time, feed into weaker earnings. The same forces that have strengthened the shekel can reverse it. A sharp correction in global equity markets, a shift in U.S. monetary policy, or renewed escalation in the region would change the balance quickly. The Bank of Israel, which holds substantial foreign exchange reserves, has so far refrained from direct intervention but retains policy tools that could alter the trajectory if needed.

For investors, the point is not to treat Israel as an isolated bet but as a form of diversification that behaves differently from the dominant exposures in most portfolios. Global allocations remain heavily concentrated in U.S. assets and the dollar. That concentration has been rewarded, but it is not without risk. Adding exposure to a market driven by export surpluses, distinct sectoral strengths, and different currency dynamics reduces that dependence.

Israel’s market is not large in global terms, but it is not peripheral either.

Its key industries sit at the center of global demand in cybersecurity, software, and defense. Its currency reflects persistent capital inflows and external surpluses. The combination creates a profile that does not move in lockstep with larger markets.

The more uncomfortable conclusion is that the very factors that deter some investors – geopolitical tension, volatility, and headline risk – are also what keep valuations from fully reflecting those fundamentals. Price them too lightly, and the risks are obvious. Price them too heavily, and the opportunity is missed.

Israel’s recent performance is not an anomaly to be explained away. It reflects deeper forces at work. The question for investors is not whether the contradiction exists, but whether they are prepared to act on it.

You might also like to read this:

")

")

")

")

")

")

")

")

fighter jet during the \"Blue Flag\", an international aerial training exercise at the Ovda air force base, Southern Israel, November 11, 2019. Photo by Yonatan Sindel/Flash90")

")